The investment landscape is shifting that a greater number of companies are now explicitly identifying and reporting on ESG while greater degrees of impact reporting, guidance and research are expanding – all to enhance views of economic materiality.

Advocating for Materiality

Materiality, the notion that specific risks or opportunities can be identified through detailed ESG analysis, can be applied in novel ways to quantify say the risks, of gender or race diversity in a firm’s board or workforce, a CEO’s pattern of ethical leadership (like Uber’s alleged harassment of women), lack of customer welfare (United Airlines’ alleged treatment of customers) or lapses in privacy and security (Yahoo’s data breach).

Matthew Weatherly-White of the Caprock Group argues that capital traditionally driven through philanthropic or consumer advocacy institutions are not sufficient to meet the demands of a world increasingly being challenged by internal risks like corporate malfeasance or outside risks such as climate change, economic automation or persistent poverty.

A number of organizations, and practitioners, are emerging to thus provide more guidance to materiality and ESG. Independent bodies have proposed new accounting standards to capture and disclose material, decision-useful information to investors.

SASB’s Materiality Map Tool

One such tool, SASB’s Materiality Map™ is based on tests designed to measure issues on behalf of the “reasonable investor.” The Map relies heavily on two types of “evidence”: evidence of investor interest, and evidence of financial impact.

Work behind the Map began by grouping 30 sustainability issues into five broad buckets: Environment, Social Capital, Human Capital, Business Model & Innovation, and Leadership & Governance.

“Evidence” was then measured through the culling of hundreds of thousands of documents including 10-Ks, media, regulatory action, CSR reports, call transcripts and many other sources, until a materiality “heatmap” emerges (see image).

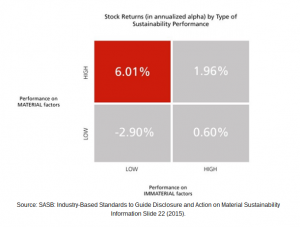

A Harvard study on linking performance of stocks to sustainability found that firms generated an annualized alpha of 6.01% (image below) on material sustainability issues, using the Sustainability Accounting Standards Board (SASB) framework. Clearly, there is value in utilizing such tools as economies of scale come into play.

***

“Many mutual funds incorporate SRI (Socially Responsible Investing) or ESG (Environmental, Social/Sustainable, Governance) factors from a values perspective. These funds utilize what is essentially an activist approach to capitalism: screening portfolios either positively or negatively to map and reflect investors’ values.

Examples include funds that avoid so-called “sin stocks” including tobacco and firearms manufacturers, or prefer companies offering progressive maternity and paternity leave benefits, or invest in companies specifically seeking to reflect gender or race diversification among their employees. While investment merit is obviously an important driver for security selection, values alignment can be equally important, leading to portfolios based on factors beyond purely financial gain.

Materiality, on the other hand, is anchored in the idea that specific risks or opportunities can be identified through sophisticated ESG analysis. This analysis can discount as obvious a risk as the imposition of a carbon-pricing mechanism, or as subtle as the importance of gender and race diversity in the boardroom, C-suite, and the employee base.

The evolution from “values” to “materiality” is an indication that the entire discipline of social and environmental investing is growing up. This maturation is reflected in the investment activity among some of the world’s wealthiest families and largest asset managers.

ESG factors have begun to be braided into core investment disciplines. Understanding, pricing, and mitigating risk. Identifying opportunity. Investing in businesses that offer products and services addressing consumer demand. These are foundational activities for any investor. That SRI/ESG factors are now integrated on the same level as enterprise valuation, free-cash-flow, and operating margins suggests that impact investing is likely to become more prevalent.

In other words, incorporating ESG factors has been proven to be good investing practice.

One thing is certain: At a time of rising climate risk and growing recognition of the corrosive effect on societies from inequalities in income, wealth, and opportunity, impact investing won’t be silenced.”

Source: Marketwatch, Caprock Group, SASB, CFA Institute

{kind=link}