Update 2026

SRI AUM reached $61.7 billion in late 2025 from $22.9 trillion in 2016, according to the GSIA Global Sustainable Investment Alliance’s biennial report. Notable growth drivers:

- In Europe 67% of asset owners citing ESG matters becoming more material to investment policy in the last five years and 46% of their assets under management integrating ESG considerations.

- In the US, domestic flows into sustainable investment strategies moderated after President Trump’s election, compared with the rapid expansion of the prior decade. Yet institutional investors continued to integrate sustainability factors into asset allocation as part of fiduciary risk management.

- In Japan, SRI reached approximately ¥626 trillion, 63.5% of total AUM, a 16.4% increase from previous years. Japan also became the world’s first sovereign issuer of climate transition bonds in 2024, signalling its commitment to financing the decarbonization in hard-to-abate sectors such as steel, chemicals, and aviation.

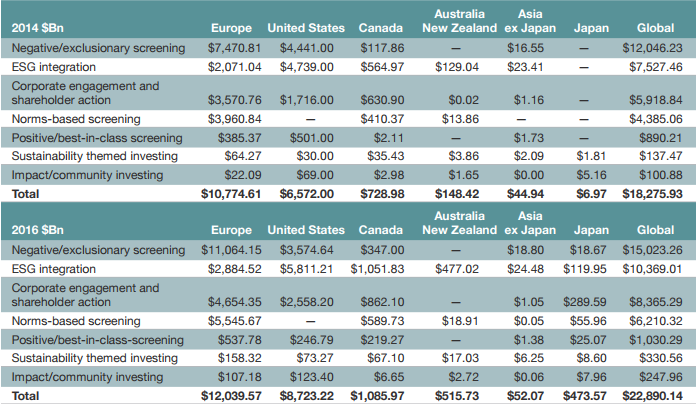

Why This Matters - Growth Compared to 2016 Among the factors cited by the report for SRI’s growth globally: Sustainable and responsible investment’s (SRI) share now stands at 26% of all professionally managed assets globally, according to the confidential survey of investment management and institutional asset firms. Impact Investing Growth While targeted private market investments were studied, community investing, where capital is specifically directed to underserved individuals or communities, was also included. Assets under management in impact investing strategies, including “community investing,” stood at $248 billion in 2016, up 147% from $101 billion in 2014; this includes retail assets. Growths by Region Growths by region were as follows: United States – SRI grew to $8.7 trillion in 2016, up by 33% from $6.6 trillion in 2014, now representing 22% of surveyed investment AUM. $8.1 trillion is managed by institutional investors, money managers and community investment institutions applying various environmental, social and governance ESG criteria in their investment analysis and portfolio selection. ESG integration, the dominant strategy, affects approximately $5.8 trillion in assets. Climate change was the most popular social good driver, and represented up to $2 trillion in assets. Europe – SRI grew to $12 trillion in 2016, up by 12% from $10.8 trillion in 2014, now representing 53% of surveyed investment AUM. Exclusionary screening and norms-based screening remain the dominant SRI strategies, and their use grew by 48% and 40% respectively, affecting up to $11 trillion in assets. Asia exc. Japan – SRI grew to $52.1 billion in 2016, up by 16% from $45 billion in 2014, growing more slowly compared to 32% growth from 2012 to 2014. Sharia-compliant AUM, represented chiefly by Malaysia, and whose investment principles are consistent with SRI, now total $18 billion. ESG integration and negative/exclusionary screening were the most popular SRI strategies, representing $24.5 billion and $18.8 billion in assets respectively. Addressable markets for sustainable investing grew fastest in China, 105%, followed by India, 104% and Pakistan, 50%, all since the start of 2014. China – of the countries surveyed in Asia, China’s SRI grew the most, to $2.9 billion, up by 157% from $450.9 million. A majority of SRI AUM were related to clean energy unsurprisingly, given the attention China’s dirty air has been receiving. The country remains committed to its promise of greener policies, thanks in large part to the previous US administration under President Obama, to curtail carbon emissions by 2030. It is expected to make further advances in climate change and environmental policy, including drafting a climate change law and establishing carbon trading regulation. Japan – SRI grew to $473.6 billion in 2016, up from $7 bilion in 2014, owing to changes in Japan’s sustainable investment market and new asset information collected by the surveys. Corporate engagement and shareholder action was the dominant SRI strategy at $289.6 billion. Canada – SRI grew to $1.08 trillion in 2016, up by 49% from $729 billion in 2014, its large growth owed mainly to the growth of pensions by 45% to $374 billion in the last two years, and whose numbers were in turn driven by Ontario Pension Benefits Act’s requirements since January 2016 to report any ESG factors in investment policies. Australia and New Zealand – SRI grew to $515.7 billion in 2016, up by 248% from $148.2 billion in 2014. In both countries combined, SRI assets now make up a substantial portion of the professional investment market in this region, including 50 percent of professionally managed assets in Australia, reflecting the region’s strong commitment to ESG integrations in investment portfolios. Africa – through data compiled from a University of Cape Town publication, South Africa holds the biggest share of total SRI AUM with $678 billion surveyed, Nigeria second $30 billion), and Kenya with $13 billion. Nearly 47% of all funds utilized one or more sustainable investing strategies. Latin America – no SRI data from surveys but indications of ESG advocacy are increasing, to name a few: Colombia’s Green Protocol, subscriptions of the Buenos Aires Stock Exchange, Santiago (Chile) Stock Exchange to and partnership by the Mexico Stock Exchange with the Sustainable Stock Exchange (SSE) Initiative, IndexAmericas. The AFORES (Private Pension Funds) in Mexico, the main domestic investors in the country, are said to be beginning to develop ESG strategies due mainly to response to international pressure, the report says. Based on these trends, and calls by influencers like the CFA Institute’s Matt Orsagh’s suggestion for a more three-dimensional approach to SRI and ESG, advisors and analysts who fail to understand the growing popularity of investing according to ESG principles risk falling behind their competition. Enclosed in quotes below from the report were definitions of the ESG strategies being adopted: “1. Negative/exclusionary screening: the exclusion from a fund or portfolio of certain sectors, companies or practices based on specific ESG criteria; 2. Positive/best-in-class screening: investment in sectors, companies or projects selected for positive ESG performance relative to industry peers; 3. Norms-based screening: screening of investments against minimum standards of business practice based on international norms; 4. ESG integration: the systematic and explicit inclusion by investment managers of environmental, social and governance factors into financial analysis; 5. Sustainability themed investing: investment in themes or assets specifically related to sustainability (for example clean energy, green technology or sustainable agriculture); 6. Impact/community investing: targeted investments, typically made in private markets, aimed at solving social or environmental problems, and including community investing, where capital is specifically directed to traditionally underserved individuals or communities, as well as financing that is provided to businesses with a clear social or environmental purpose; and 7. Corporate engagement and shareholder action: the use of shareholder power to influence corporate behavior, including through direct corporate engagement (i.e., communicating with senior management and/or boards of companies), filing or co-filing shareholder proposals, and proxy voting that is guided by comprehensive ESG guidelines.” Read More at GSI Alliance

Global assets professionally managed under sustainable and responsible investment (SRI) strategies grew by a compound annual growth rate of 11.9% and in 2016 had reached $22.9 trillion AUM from $18.3 trillion in 2014, according to GSIA Global Sustainable Investment Alliance’s biennial report then.